The best travel insurance policies and providers

It's easy to dismiss the value of travel insurance until you need it.

Many travelers have strong opinions about whether you should buy travel insurance . However, the purpose of this post isn't to determine whether it's worth investing in. Instead, it compares some of the top travel insurance providers and policies so you can determine which travel insurance option is best for you.

Of course, as the coronavirus remains an ongoing concern, it's important to understand whether travel insurance covers pandemics. Some policies will cover you if you're diagnosed with COVID-19 and have proof of illness from a doctor. Others will take coverage a step further, covering additional types of pandemic-related expenses and cancellations.

Know, though, that every policy will have exclusions and restrictions that may limit coverage. For example, fear of travel is generally not a covered reason for invoking trip cancellation or interruption coverage, while specific stipulations may apply to elevated travel warnings from the Centers for Disease Control and Prevention.

Interested in travel insurance? Visit InsureMyTrip.com to shop for plans that may fit your travel needs.

So, before buying a specific policy, you must understand the full terms and any special notices the insurer has about COVID-19. You may even want to buy the optional cancel for any reason add-on that's available for some comprehensive policies. While you'll pay more for that protection, it allows you to cancel your trip for any reason and still get some of your costs back. Note that this benefit is time-sensitive and has other eligibility requirements, so not all travelers will qualify.

In this guide, we'll review several policies from top travel insurance providers so you have a better understanding of your options before picking the policy and provider that best address your wants and needs.

The best travel insurance providers

To put together this list of the best travel insurance providers, a number of details were considered: favorable ratings from TPG Lounge members, the availability of details about policies and the claims process online, positive online ratings and the ability to purchase policies in most U.S. states. You can also search for options from these (and other) providers through an insurance comparison site like InsureMyTrip .

When comparing insurance providers, I priced out a single-trip policy for each provider for a $2,000, one-week vacation to Istanbul . I used my actual age and state of residence when obtaining quotes. As a result, you may see a different price — or even additional policies due to regulations for travel insurance varying from state to state — when getting a quote.

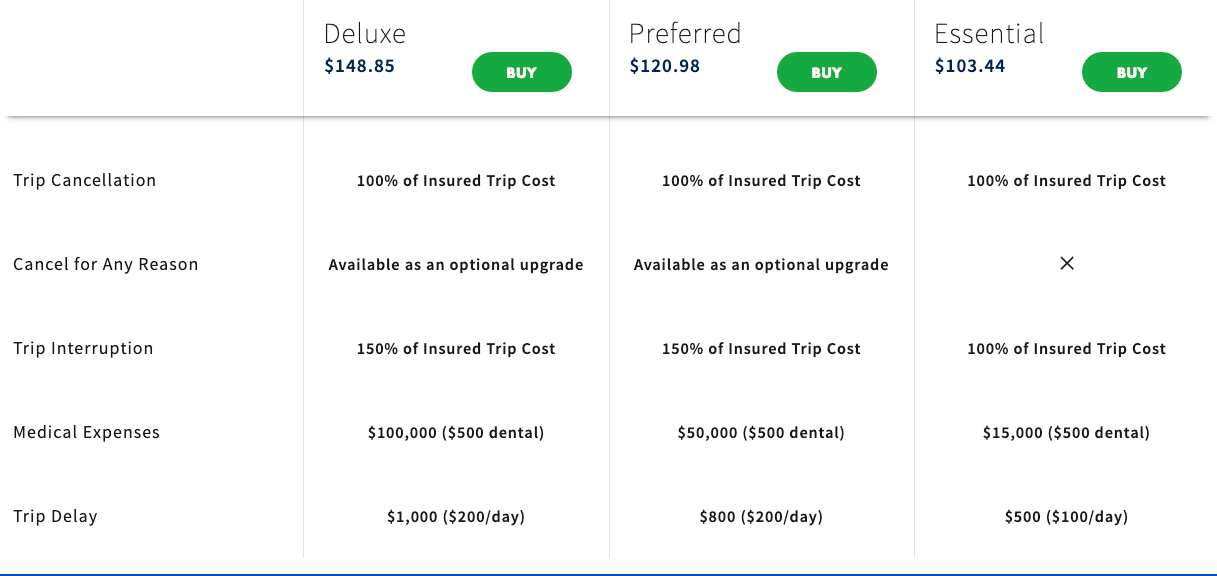

AIG Travel Guard

AIG Travel Guard receives many positive reviews from readers in the TPG Lounge who have filed claims with the company. AIG offers three plans online, which you can compare side by side, and the ability to examine sample policies. Here are three plans for my sample trip to Turkey.

AIG Travel Guard also offers an annual travel plan. This plan is priced at $259 per year for one Florida resident.

Additionally, AIG Travel Guard offers several other policies, including a single-trip policy without trip cancellation protection . See AIG Travel Guard's COVID-19 notification and COVID-19 advisory for current details regarding COVID-19 coverage.

Preexisting conditions

Typically, AIG Travel Guard wouldn't cover you for any loss or expense due to a preexisting medical condition that existed within 180 days of the coverage effective date. However, AIG Travel Guard may waive the preexisting medical condition exclusion on some plans if you meet the following conditions:

- You purchase the plan within 15 days of your initial trip payment.

- The amount of coverage you purchase equals all trip costs at the time of purchase. You must update your coverage to insure the costs of any subsequent arrangements that you add to your trip within 15 days of paying the travel supplier for these additional arrangements.

- You must be medically able to travel when you purchase your plan.

Standout features

- The Deluxe and Preferred plans allow you to purchase an upgrade that lets you cancel your trip for any reason. However, reimbursement under this coverage will not exceed 50% or 75% of your covered trip cost.

- You can include one child (age 17 and younger) with each paying adult for no additional cost on most single-trip plans.

- Other optional upgrades, including an adventure sports bundle, a baggage bundle, an inconvenience bundle, a pet bundle, a security bundle and a wedding bundle, are available on some policies. So, an AIG Travel Guard plan may be a good choice if you know you want extra coverage in specific areas.

Purchase your policy here: AIG Travel Guard .

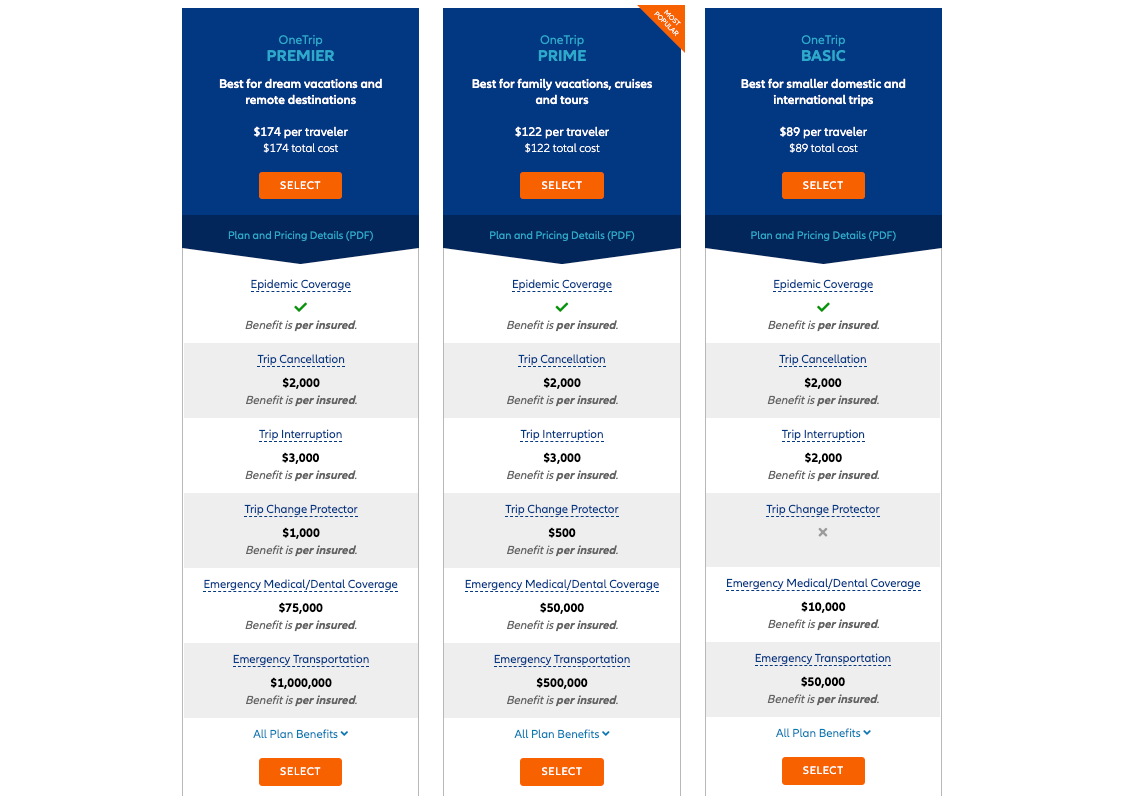

Allianz Travel Insurance

Allianz is one of the most highly regarded providers in the TPG Lounge, and many readers found the claim process reasonable. Allianz offers many plans, including the following single-trip plans for my sample trip to Turkey.

If you travel frequently, it may make sense to purchase an annual multi-trip policy. For this plan, all of the maximum coverage amounts in the table below are per trip (except for the trip cancellation and trip interruption amounts, which are an aggregate limit per policy). Trips typically must last no more than 45 days, although some plans may cover trips of up to 90 days.

See Allianz's coverage alert for current information on COVID-19 coverage.

Most Allianz travel insurance plans may cover preexisting medical conditions if you meet particular requirements. For the OneTrip Premier, Prime and Basic plans, the requirements are as follows:

- You purchased the policy within 14 days of the date of the first trip payment or deposit.

- You were a U.S. resident when you purchased the policy.

- You were medically able to travel when you purchased the policy.

- On the policy purchase date, you insured the total, nonrefundable cost of your trip (including arrangements that will become nonrefundable or subject to cancellation penalties before your departure date). If you incur additional nonrefundable trip expenses after purchasing this policy, you must insure them within 14 days of their purchase.

- Allianz offers reasonably priced annual policies for independent travelers and families who take multiple trips lasting up to 45 days (or 90 days for select plans) per year.

- Some Allianz plans provide the option of receiving a flat reimbursement amount without receipts for trip delay and baggage delay claims. Of course, you can also submit receipts to get up to the maximum refund.

- For emergency transportation coverage, you or someone on your behalf must contact Allianz, and Allianz must then make all transportation arrangements in advance. However, most Allianz policies provide an option if you cannot contact the company: Allianz will pay up to what it would have paid if it had made the arrangements.

Purchase your policy here: Allianz Travel Insurance .

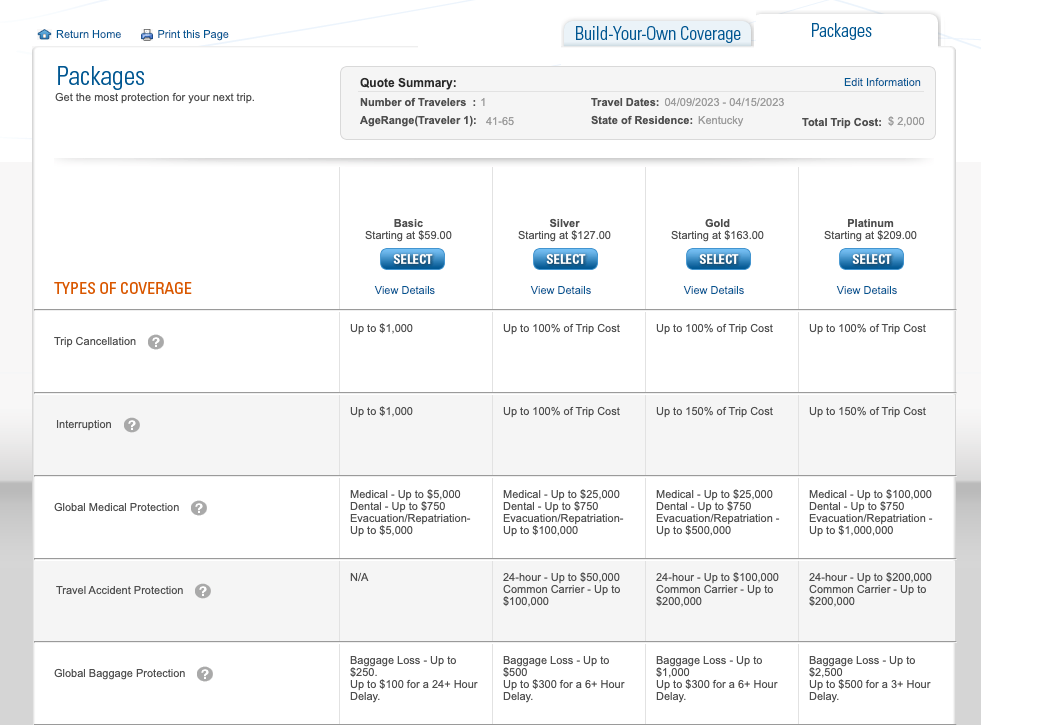

American Express Travel Insurance

American Express Travel Insurance offers four different package plans and a build-your-own coverage option. You don't have to be an American Express cardholder to purchase this insurance. Here are the four package options for my sample weeklong trip to Turkey. Unlike some other providers, Amex won't ask for your travel destination on the initial quote (but will when you purchase the plan).

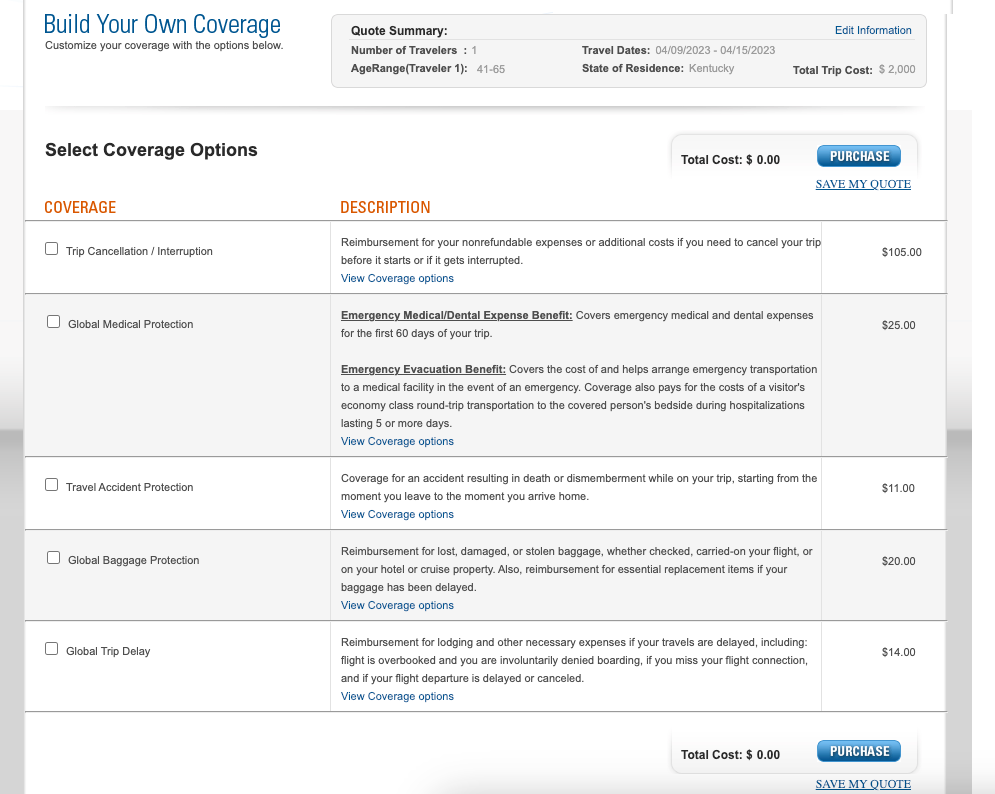

Amex's build-your-own coverage plan is unique because you can purchase just the coverage you need. For most types of protection, you can even select the coverage amount that works best for you.

The prices for the packages and the build-your-own plan don't increase for longer trips — as long as the trip cost remains constant. However, the emergency medical and dental benefit is only available for your first 60 days of travel.

Typically, Amex won't cover any loss you incur because of a preexisting medical condition that existed within 90 days of the coverage effective date. However, Amex may waive its preexisting-condition exclusion if you meet both of the following requirements:

- You must be medically able to travel at the time you pay the policy premium.

- You pay the policy premium within 14 days of making the first covered trip deposit.

- Amex's build-your-own coverage option allows you to only purchase — and pay for — the coverage you need.

- Coverage on long trips doesn't cost more than coverage for short trips, making this policy ideal for extended getaways. However, the emergency medical and dental benefit only covers your first 60 days of travel.

- American Express Travel Insurance can protect travel expenses you purchase with Amex Membership Rewards points in the Pay with Points program (as well as travel expenses bought with cash, debit or credit). However, travel expenses bought with other types of points and miles aren't covered.

Purchase your policy here: American Express Travel Insurance .

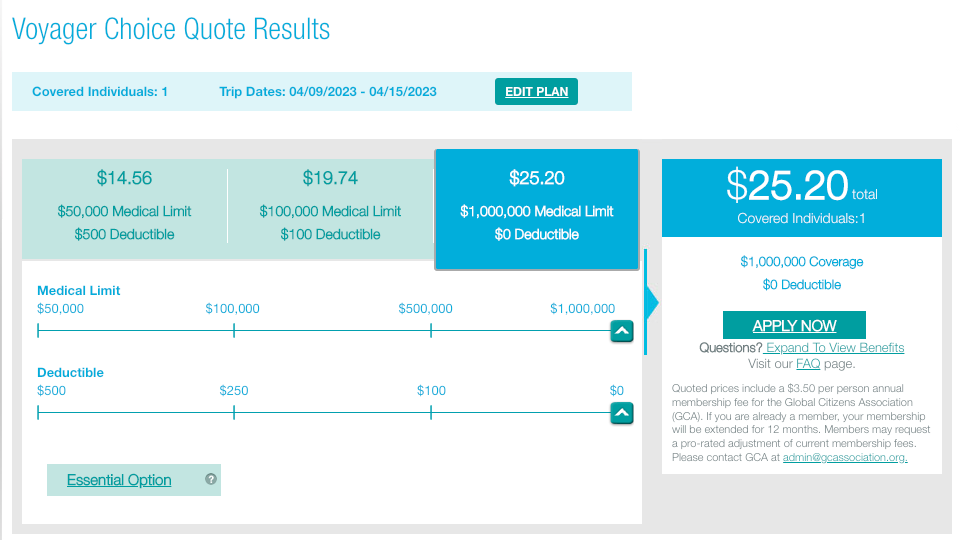

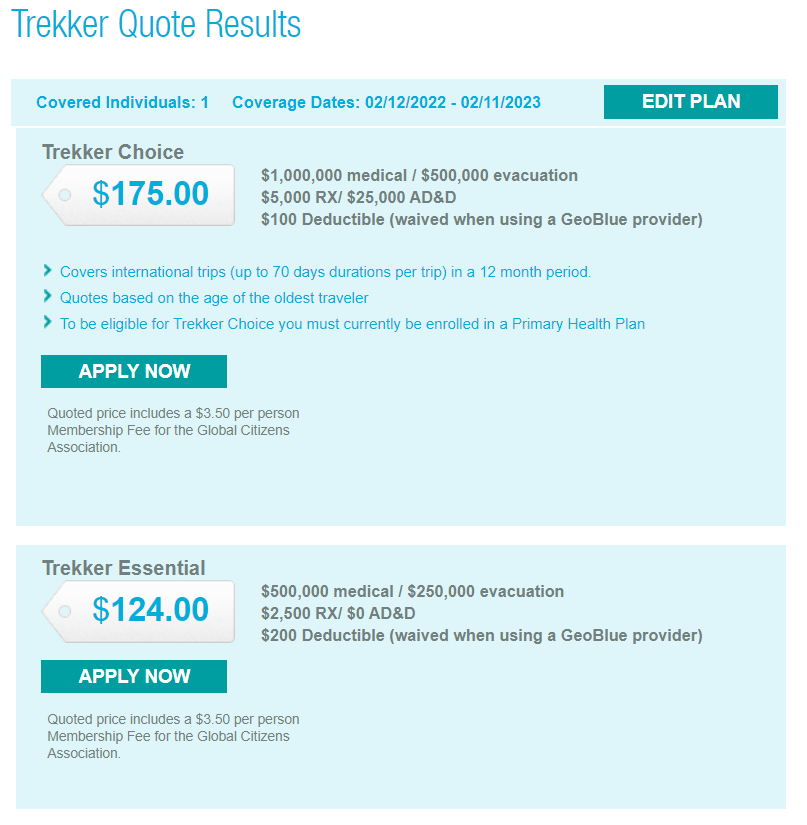

GeoBlue is different from most other providers described in this piece because it only provides medical coverage while you're traveling internationally and does not offer benefits to protect the cost of your trip. There are many different policies. Some require you to have primary health insurance in the U.S. (although it doesn't need to be provided by Blue Cross Blue Shield), but all of them only offer coverage while traveling outside the U.S.

Two single-trip plans are available if you're traveling for six months or less. The Voyager Choice policy provides coverage (including medical services and medical evacuation for a sudden recurrence of a preexisting condition) for trips outside the U.S. to travelers who are 95 or younger and already have a U.S. health insurance policy.

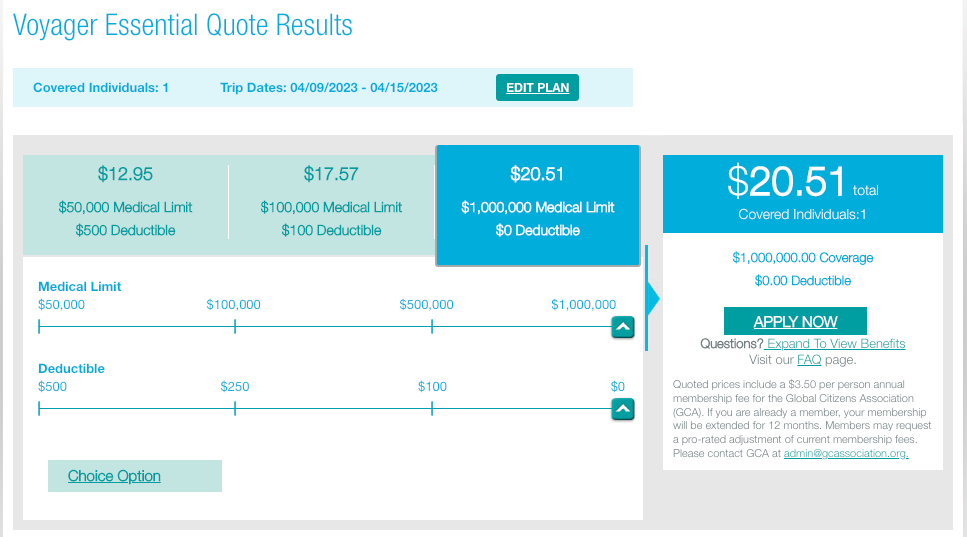

The Voyager Essential policy provides coverage (including medical evacuation for a sudden recurrence of a preexisting condition) for trips outside the U.S. to travelers who are 95 or younger, regardless of whether they have primary health insurance.

In addition to these options, two multi-trip plans cover trips of up to 70 days each for one year. Both policies provide coverage (including medical services and medical evacuation for preexisting conditions) to travelers with primary health insurance.

Be sure to check out GeoBlue's COVID-19 notices before buying a plan.

Most GeoBlue policies explicitly cover sudden recurrences of preexisting conditions for medical services and medical evacuation.

- GeoBlue can be an excellent option if you're mainly concerned about the medical side of travel insurance.

- GeoBlue provides single-trip, multi-trip and long-term medical travel insurance policies for many different types of travel.

Purchase your policy here: GeoBlue .

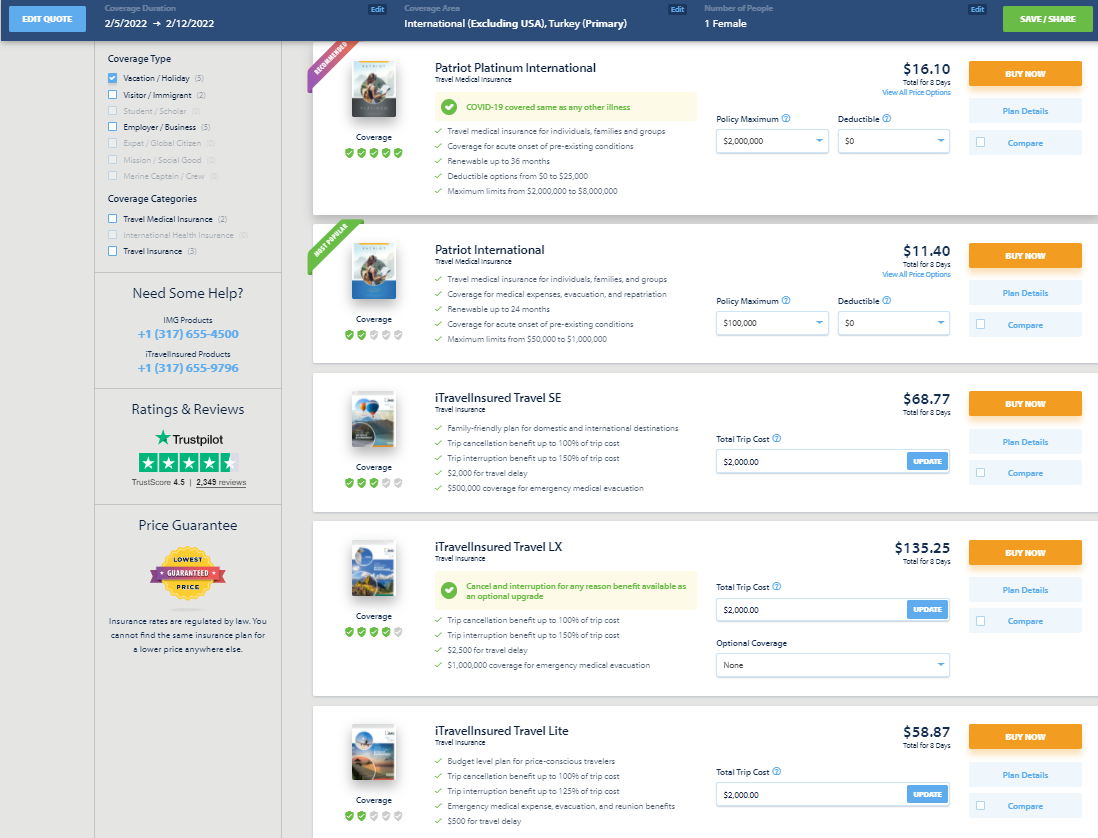

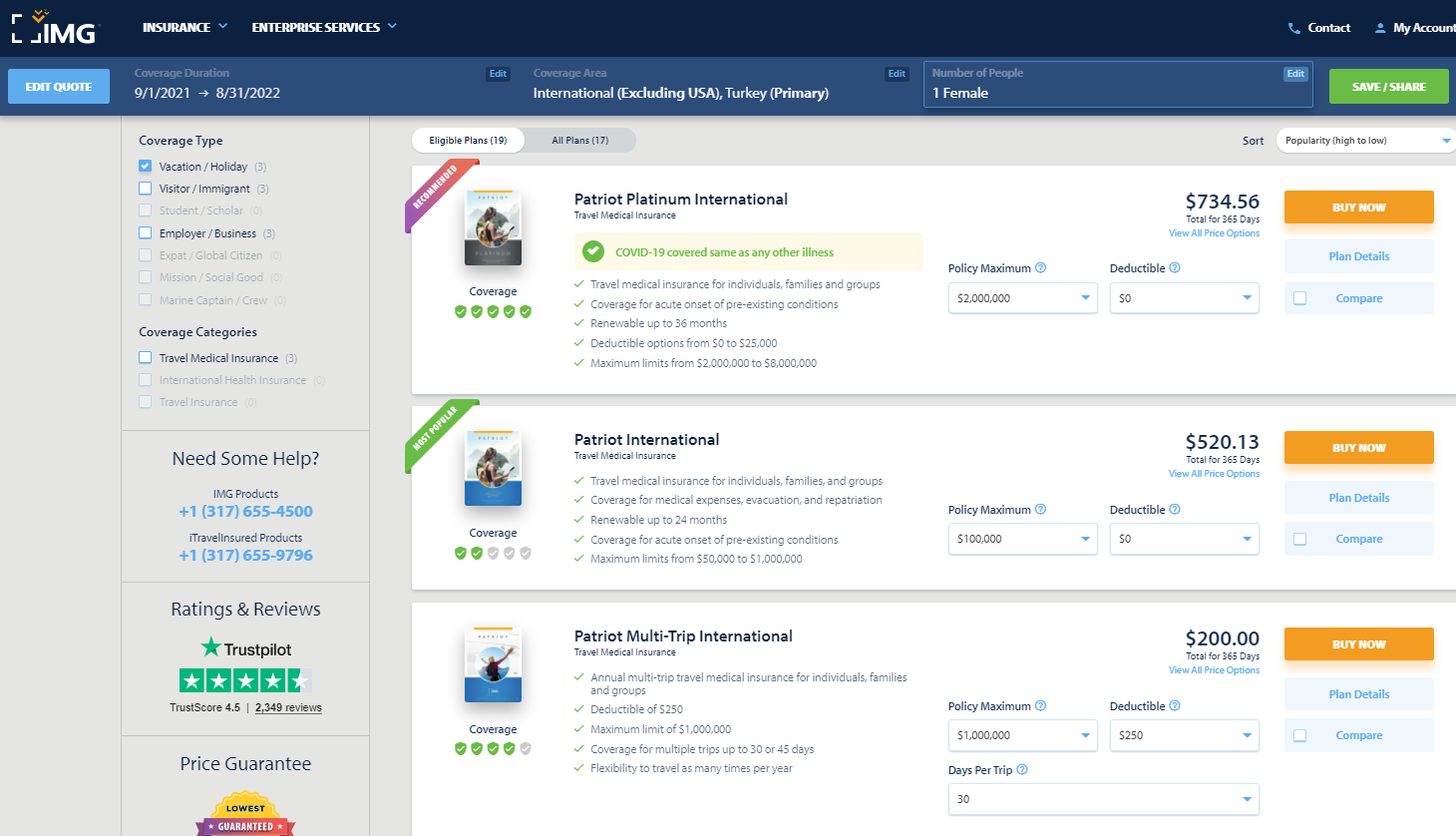

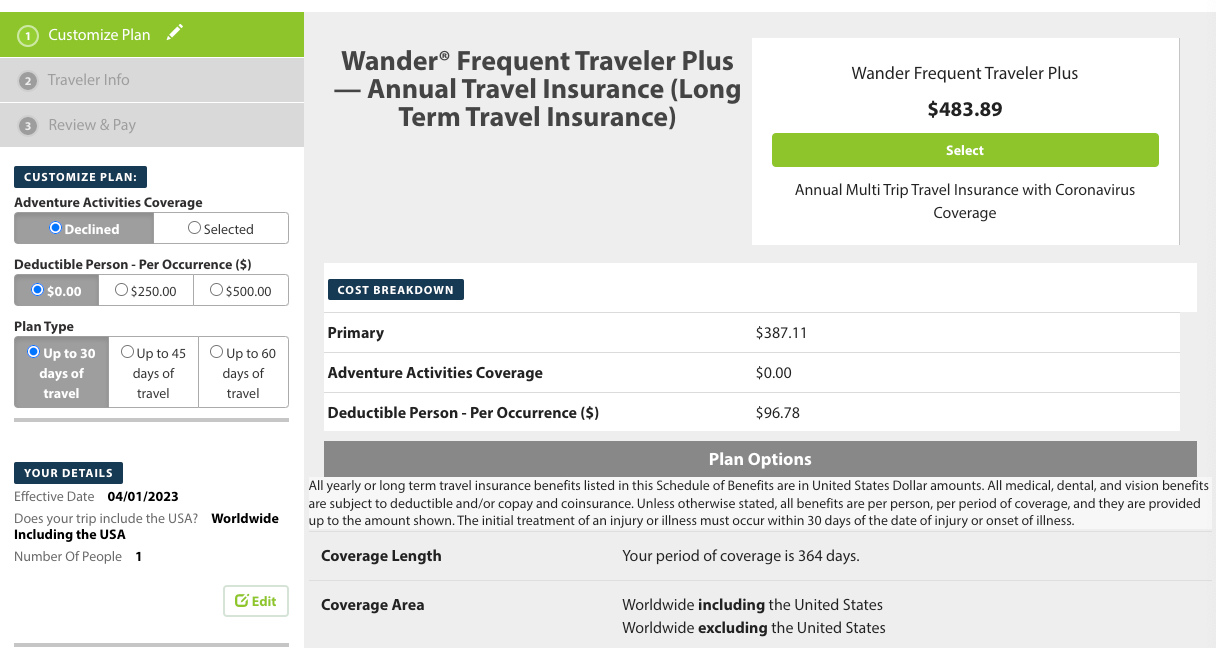

IMG offers various travel medical insurance policies for travelers, as well as comprehensive travel insurance policies. For a single trip of 90 days or less, there are five policy types available for vacation or holiday travelers. Although you must enter your gender, males and females received the same quote for my one-week search.

You can purchase an annual multi-trip travel medical insurance plan. Some only cover trips lasting up to 30 or 45 days, but others provide coverage for longer trips.

See IMG's page on COVID-19 for additional policy information as it relates to coronavirus-related claims.

Most plans may cover preexisting conditions under set parameters or up to specific amounts. For example, the iTravelInsured Travel LX travel insurance plan shown above may cover preexisting conditions if you purchase the insurance within 24 hours of making the final payment for your trip.

For the travel medical insurance plans shown above, preexisting conditions are covered for travelers younger than 70. However, coverage is capped based on your age and whether you have a primary health insurance policy.

- Some annual multi-trip plans are modestly priced.

- iTravelInsured Travel LX may offer optional cancel for any reason and interruption for any reason coverage, if eligible.

Purchase your policy here: IMG .

Travelex Insurance

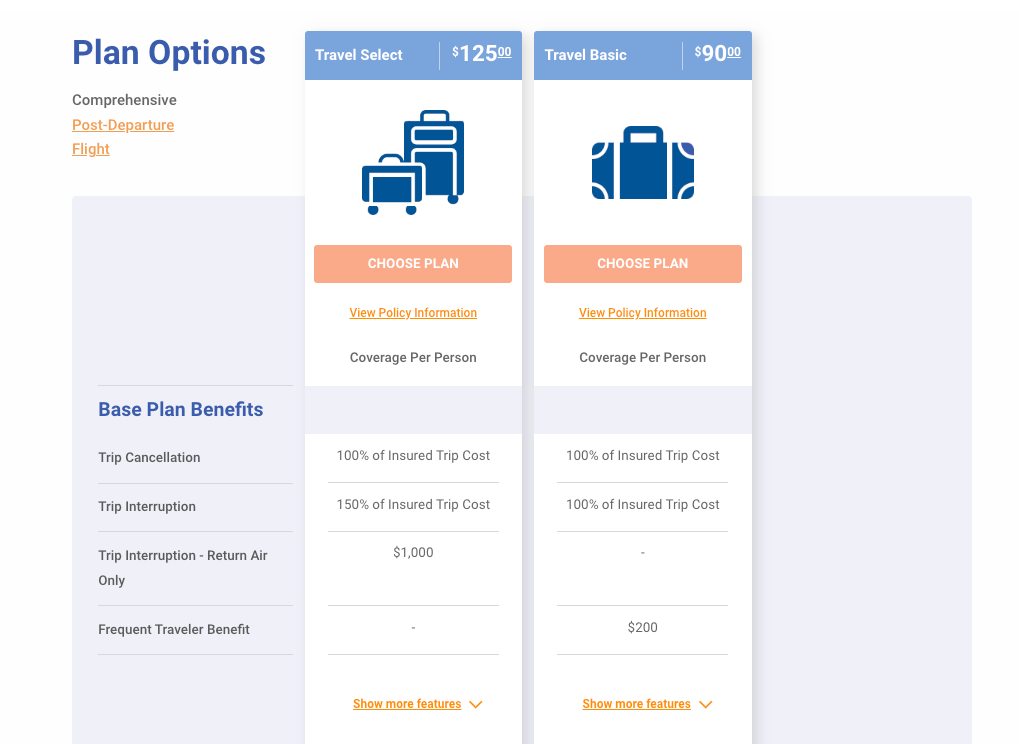

Travelex offers three single-trip plans: Travel Basic, Travel Select and Travel America. However, only the Travel Basic and Travel Select plans would be applicable for my trip to Turkey.

See Travelex's COVID-19 coverage statement for coronavirus-specific information.

Typically, Travelex won't cover losses incurred because of a preexisting medical condition that existed within 60 days of the coverage effective date. However, the Travel Select plan may offer a preexisting condition exclusion waiver. To be eligible for this waiver, the insured traveler must meet all the following conditions:

- You purchase the plan within 15 days of the initial trip payment.

- The amount of coverage purchased equals all prepaid, nonrefundable payments or deposits applicable to the trip at the time of purchase. Additionally, you must insure the costs of any subsequent arrangements added to the same trip within 15 days of payment or deposit.

- All insured individuals are medically able to travel when they pay the plan cost.

- The trip cost does not exceed the maximum trip cost limit under trip cancellation as shown in the schedule per person (only applicable to trip cancellation, interruption and delay).

- Travelex's Travel Select policy can cover trips lasting up to 364 days, which is longer than many single-trip policies.

- Neither Travelex policy requires receipts for trip and baggage delay expenses less than $25.

- For emergency evacuation coverage, you or someone on your behalf must contact Travelex and have Travelex make all transportation arrangements in advance. However, both Travelex policies provide an option if you cannot contact Travelex: Travelex will pay up to what it would have paid if it had made the arrangements.

Purchase your policy here: Travelex Insurance .

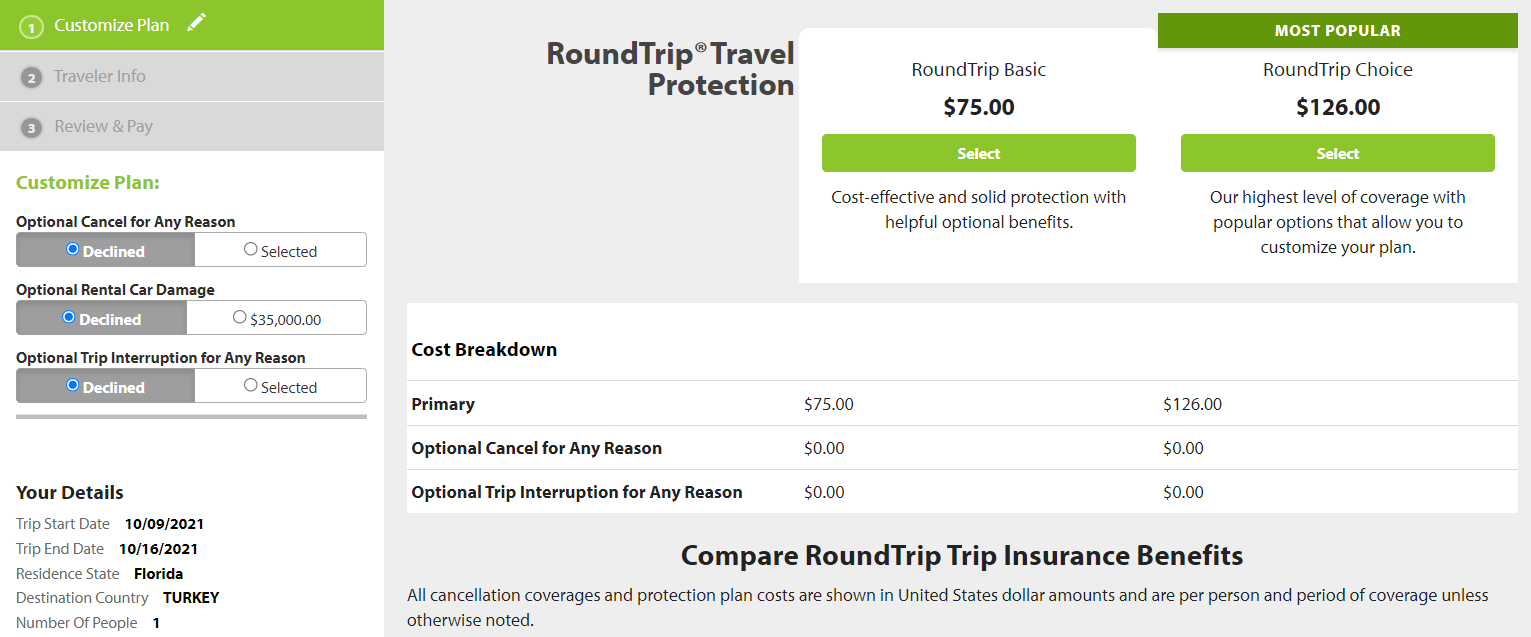

Seven Corners

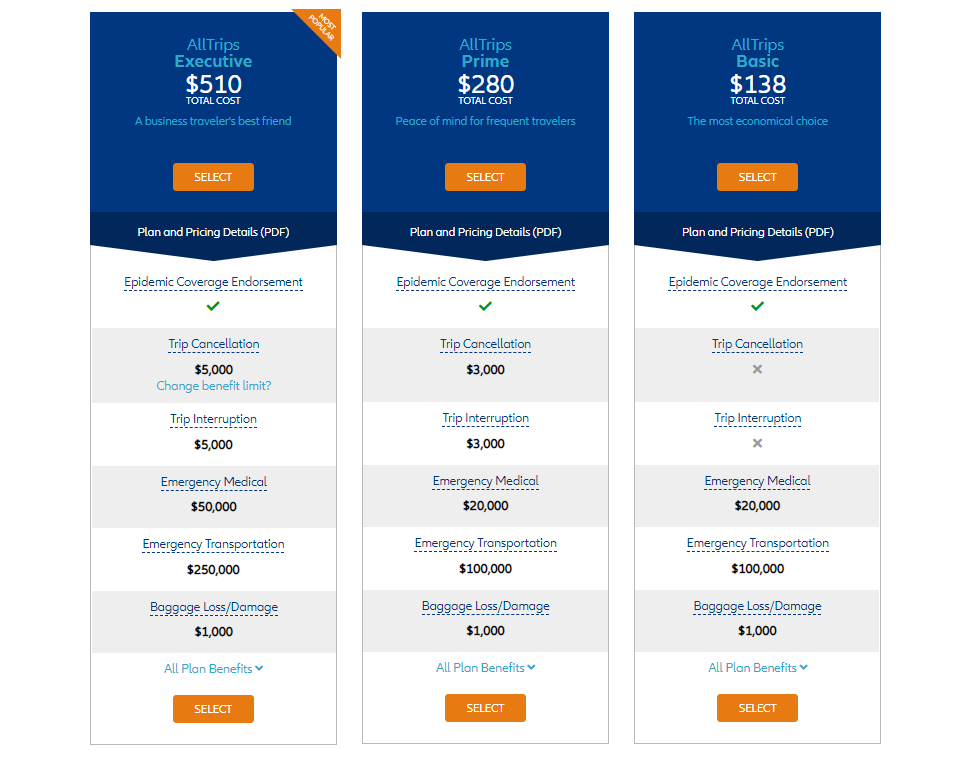

Seven Corners offers a wide variety of policies. Here are the policies that are most applicable to travelers on a single international trip.

Seven Corners also offers many other types of travel insurance, including an annual multi-trip plan. You can choose coverage for trips of up to 30, 45 or 60 days when purchasing an annual multi-trip plan.

See Seven Corner's page on COVID-19 for additional policy information as it relates to coronavirus-related claims.

Typically, Seven Corners won't cover losses incurred because of a preexisting medical condition. However, the RoundTrip Choice plan offers a preexisting condition exclusion waiver. To be eligible for this waiver, you must meet all of the following conditions:

- You buy this plan within 20 days of making your initial trip payment or deposit.

- You or your travel companion are medically able and not disabled from travel when you pay for this plan or upgrade your plan.

- You update the coverage to include the additional cost of subsequent travel arrangements within 15 days of paying your travel supplier for them.

- Seven Corners offers the ability to purchase optional sports and golf equipment coverage. If purchased, this extra insurance will reimburse you for the cost of renting sports or golf equipment if yours is lost, stolen, damaged or delayed by a common carrier for six or more hours. However, Seven Corners must authorize the expenses in advance.

- You can add cancel for any reason coverage or trip interruption for any reason coverage to RoundTrip plans. Although some other providers offer cancel for any reason coverage, trip interruption for any reason coverage is less common.

- Seven Corners' RoundTrip Choice policy offers a political or security evacuation benefit that will transport you to the nearest safe place or your residence under specific conditions. You can also add optional event ticket registration fee protection to the RoundTrip Choice policy.

Purchase your policy here: Seven Corners .

World Nomads

World Nomads is popular with younger, active travelers because of its flexibility and adventure-activities coverage on the Explorer plan. Unlike many policies offered by other providers, you don't need to estimate prepaid costs when purchasing the insurance to have access to trip interruption and cancellation insurance.

World Nomads offers two single-trip plans.

World Nomads has a page dedicated to coronavirus coverage , so be sure to view it before buying a policy.

World Nomads won't cover losses incurred because of a preexisting medical condition (except emergency evacuation and repatriation of remains) that existed within 90 days of the coverage effective date. Unlike many other providers, World Nomads doesn't offer a waiver.

- World Nomads' policies cover more adventure sports than most providers, so activities such as bungee jumping are included. The Explorer policy covers almost any adventure sport, including skydiving, stunt flying and caving. So, if you partake in adventure sports while traveling, the Explorer policy may be a good fit.

- World Nomads' policies provide nonmedical evacuation coverage for transportation expenses if there is civil or political unrest in the country you are visiting. The coverage may also transport you home if there is an eligible natural disaster or a government expels you.

Purchase your policy here: World Nomads .

Other options for buying travel insurance

This guide details the policies of eight providers with the information available at the time of publication. There are many options when it comes to travel insurance, though. To compare different policies quickly, you can use a travel insurance aggregator like InsureMyTrip to search. Just note that these search engines won't show every policy and every provider, and you should still research the provided policies to ensure the coverage fits your trip and needs.

You can also purchase a plan through various membership associations, such as USAA, AAA or Costco. Typically, these organizations partner with a specific provider, so if you are a member of any of these associations, you may want to compare the policies offered through the organization with other policies to get the best coverage for your trip.

Related: Should you get travel insurance if you have credit card protection?

Is travel insurance worth getting?

Whether you should purchase travel insurance is a personal decision. Suppose you use a credit card that provides travel insurance for most of your expenses and have medical insurance that provides adequate coverage abroad. In that case, you may be covered enough on most trips to forgo purchasing travel insurance.

However, suppose your medical insurance won't cover you at your destination and you can't comfortably cover a sizable medical evacuation bill or last-minute flight home . In that case, you should consider purchasing travel insurance. If you travel frequently, buying an annual multi-trip policy may be worth it.

What is the best COVID-19 travel insurance?

There are various aspects to keep in mind in the age of COVID-19. Consider booking travel plans that are fully refundable or have modest change or cancellation fees so you don't need to worry about whether your policy will cover trip cancellation. This is important since many standard comprehensive insurance policies won't reimburse your insured expenses in the event of cancellation if it's related to the fear of traveling due to COVID-19.

However, if you book a nonrefundable trip and want to maintain the ability to get reimbursed (up to 75% of your insured costs) if you choose to cancel, you should consider buying a comprehensive travel insurance policy and then adding optional cancel for any reason protection. Just note that this benefit is time-sensitive and has eligibility requirements, so not all travelers will qualify.

Providers will often require CFAR purchasers insure the entire dollar amount of their travels to receive the coverage. Also, many CFAR policies mandate that you must cancel your plans and notify all travel suppliers at least 48 hours before your scheduled departure.

Likewise, if your primary health insurance won't cover you while on your trip, it's essential to consider whether medical expenses related to COVID-19 treatment are covered. You may also want to consider a MedJet medical transport membership if your trip is to a covered destination for coronavirus-related evacuation.

Ultimately, the best pandemic travel insurance policy will depend on your trip details, travel concerns and your willingness to self-insure. Just be sure to thoroughly read and understand any terms or exclusions before purchasing.

What are the different types of travel insurance?

Whether you purchase a comprehensive travel insurance policy or rely on the protections offered by select credit cards, you may have access to the following types of coverage:

- Baggage delay protection may reimburse for essential items and clothing when a common carrier (such as an airline) fails to deliver your checked bag within a set time of your arrival at a destination. Typically, you may be reimbursed up to a particular amount per incident or per day.

- Lost/damaged baggage protection may provide reimbursement to replace lost or damaged luggage and items inside that luggage. However, valuables and electronics usually have a relatively low maximum benefit.

- Trip delay reimbursement may provide reimbursement for necessary items, food, lodging and sometimes transportation when you're delayed for a substantial time while traveling on a common carrier such as an airline. This insurance may be beneficial if weather issues (or other covered reasons for which the airline usually won't provide compensation) delay you.

- Trip cancellation and interruption protection may provide reimbursement if you need to cancel or interrupt your trip for a covered reason, such as a death in your family or jury duty.

- Medical evacuation insurance can arrange and pay for medical evacuation if deemed necessary by the insurance provider and a medical professional. This coverage can be particularly valuable if you're traveling to a region with subpar medical facilities.

- Travel accident insurance may provide a payment to you or your beneficiary in the case of your death or dismemberment.

- Emergency medical insurance may provide payment or reimburse you if you must seek medical care while traveling. Some plans only cover emergency medical care, but some also cover other types of medical care. You may need to pay a deductible or copay.

- Rental car coverage may provide a collision damage waiver when renting a car. This waiver may reimburse for collision damage or theft up to a set amount. Some policies also cover loss-of-use charges assessed by the rental company and towing charges to take the vehicle to the nearest qualified repair facility. You generally need to decline the rental company's collision damage waiver or similar provision to be covered.

Should I buy travel health insurance?

If you purchase travel with credit cards that provide various trip protections, you may not see much need for additional travel insurance. However, you may still wonder whether you should buy travel medical insurance.

If your primary health insurance covers you on your trip, you may not need travel health insurance. Your domestic policy may not cover you outside the U.S., though, so it's worth calling the number on your health insurance card if you have coverage questions. If your primary health insurance wouldn't cover you, it's likely worth purchasing travel medical insurance. After all, as you can see above, travel medical insurance is often very modestly priced.

How much does travel insurance cost?

Travel insurance costs depend on various factors, including the provider, the type of coverage, your trip cost, your destination, your age, your residency and how many travelers you want to insure. That said, a standard travel insurance plan will generally set you back somewhere between 4% and 10% of your total trip cost. However, this can get lower for more basic protections or become even higher if you include add-ons like cancel for any reason protection.

The best way to determine how much travel insurance will cost is to price out your trip with a few providers discussed in the guide. Or, visit an insurance aggregator like InsureMyTrip to quickly compare options across multiple providers.

When and how to get travel insurance

For the most robust selection of available travel insurance benefits — including time-sensitive add-ons like CFAR protection and waivers of preexisting conditions for eligible travelers — you should ideally purchase travel insurance on the same day you make your first payment toward your trip.

However, many plans may still offer a preexisting conditions waiver for those who qualify if you buy your travel insurance within 14 to 21 days of your first trip expense or deposit (this time frame may vary by provider). If you don't need a preexisting conditions waiver or aren't interested in CFAR coverage, you can purchase travel insurance once your departure date nears.

You must purchase coverage before it's needed. Some travel medical plans are available for purchase after you have departed, but comprehensive plans that include medical coverage must be purchased before departing.

Additionally, you can't buy any medical coverage once you require medical attention. The same applies to all travel insurance coverage. Once you recognize the need, it's too late to protect your trip.

Once you've shopped around and decided upon the best travel insurance plan for your trip, you should be able to complete your purchase online. You'll usually be able to download your insurance card and the complete policy shortly after the transaction is complete.

Related: 7 times your credit card's travel insurance might not cover you

Bottom line

Not all travel insurance policies and providers are equal. Before buying a plan, read and understand the policy documents. By doing so, you can choose a plan that's appropriate for you and your trip — including the features that matter most to you.

For example, if you plan to go skiing or rock climbing, make sure the policy you buy doesn't contain exclusions for these activities. Likewise, if you're making two back-to-back trips during which you'll be returning home for a short time in between, be sure the plan doesn't terminate coverage at the end of your first trip.

If you're looking to cover a sudden recurrence of a preexisting condition, select a policy with a preexisting condition waiver and fulfill the requirements for the waiver. After all, buying insurance won't help if your policy doesn't cover your losses.

Disclaimer : This information is provided by IMT Services, LLC ( InsureMyTrip.com ), a licensed insurance producer (NPN: 5119217) and a member of the Tokio Marine HCC group of companies. IMT's services are only available in states where it is licensed to do business and the products provided through InsureMyTrip.com may not be available in all states. All insurance products are governed by the terms in the applicable insurance policy, and all related decisions (such as approval for coverage, premiums, commissions and fees) and policy obligations are the sole responsibility of the underwriting insurer. The information on this site does not create or modify any insurance policy terms in any way. For more information, please visit www.insuremytrip.com .

Honeymoon Travel Insurance: A Guide to Protecting Your Trip

Posted In: Honeymoon Planning

By Jim Campbell | Updated on February 7, 2024

Planning a honeymoon is an exciting phase for any couple. Amidst selecting the perfect destination, booking flights, and reserving accommodations, it’s crucial not to overlook one key aspect: honeymoon travel insurance. This article delves into why honeymoon travel insurance is essential, what it covers, and how to choose the best policy for your romantic getaway.

Choosing the right travel insurance for your honeymoon is crucial, and TravelInsurance.com offers an exceptionally user-friendly platform for comparing quotes. This site stands out because it aggregates policies from numerous top-rated insurance providers, enabling you to quickly view and compare a wide range of options side-by-side. This comprehensive comparison not only saves time but also helps ensure that you find a policy that best matches your specific needs and budget. With features like easy-to-understand breakdowns of coverage details and customer reviews, TravelInsurance.com simplifies the decision-making process. Furthermore, their user-friendly interface and secure online purchase process mean that you can select and buy your ideal travel insurance policy with confidence and ease, ensuring your honeymoon is safeguarded against unforeseen events.

Why Honeymoon Travel Insurance is Essential

Peace of mind on your special trip.

Honeymoons are meant to be blissful and stress-free. However, unforeseen events like flight cancellations, medical emergencies, or lost luggage can quickly turn your dream vacation into a nightmare. Honeymoon travel insurance provides a safety net, ensuring you’re not left stranded or out of pocket due to unexpected circumstances.

Protecting Your Investment

Weddings and honeymoons are significant investments. With travel insurance, you protect this investment. If you need to cancel or cut your trip short due to emergencies, a good policy can cover non-refundable costs, allowing you to plan a redo without financial strain.

What Does Honeymoon Travel Insurance Cover?

Trip cancellation and interruption.

This covers you if you need to cancel or interrupt your trip due to unforeseen events like illness, injury, or other emergencies.

Medical Emergencies

Overseas medical treatment can be costly. Travel insurance covers medical expenses, ensuring you get the care you need without a hefty bill.

Lost or Stolen Luggage

Losing your belongings is distressing, especially on a honeymoon. Travel insurance can reimburse you for lost, stolen, or damaged luggage.

Travel Delays and Missed Connections

Delays can disrupt your plans. Insurance can cover additional accommodation costs and rearrange travel plans.

Choosing the Right Honeymoon Travel Insurance

Assess your needs.

Consider the nature of your trip. Are you going on a cruise, a remote island, or a city break? Different trips require different coverages.

Read the Fine Print

Understand what is and isn’t covered. Some policies may not cover extreme sports or pre-existing medical conditions.

Compare Quotes

Get quotes from multiple insurers to find the best coverage at the most reasonable price. Look beyond price; consider coverage limits, deductibles, and customer reviews.

Consider a Combined Policy

If you already have wedding insurance, some providers might offer a combined policy for both the wedding and honeymoon, potentially saving you money.

Honeymoon travel insurance is an essential aspect of planning your romantic getaway. It offers peace of mind, financial protection, and ensures that unexpected events don’t dampen the most special trip of your life. By choosing the right policy, you can focus on making unforgettable memories with your partner.

Honeymoon Travel Insurance FAQs

Absolutely. While no one anticipates mishaps during their honeymoon, travel insurance provides a layer of protection against unforeseen events. It covers losses due to trip cancellations, medical emergencies, lost luggage, and other unexpected occurrences, ensuring that you’re safeguarded financially and can enjoy your honeymoon with peace of mind.

While the basic premise is similar, honeymoon travel insurance may offer additional coverages tailored for couples. This could include enhanced trip interruption coverage or special provisions for activities typically enjoyed on honeymoons.

It’s best to purchase travel insurance soon after booking your trip. This ensures that you’re covered for any cancellations or changes that might occur from the time of booking until your departure.

Yes, but you need to make sure your policy covers specific activities you’re planning, like scuba diving, hiking, or skiing. Some insurers offer customizable policies that allow you to add coverage for adventure sports.

This depends on the policy. Some travel insurance policies cover pre-existing conditions if you purchase the insurance within a certain period after making your initial trip deposit. Always disclose any pre-existing conditions when purchasing your policy to understand your coverage.

Research and compare different providers. We recommend using TravelInsurance.com. Look at customer reviews, the ease of making claims, and the clarity of their policy information. Price is important, but it shouldn’t be the only factor in your decision.

Typically, you’ll need documentation related to your claim, such as medical records for medical claims, police reports for theft, or communication from airlines for trip delays. Always keep detailed records and receipts during your trip.

Some policies offer ‘Cancel For Any Reason’ (CFAR) coverage, which allows you to cancel your trip for reasons not typically covered under standard cancellation policies. This coverage is usually an add-on and might cost more.

The cost varies based on factors like the length of your trip, your destination, the total cost of your trip, and the coverage you choose. Generally, travel insurance costs between 4% to 10% of your total trip cost.

About The Author

Jim Campbell

Jim is the owner of Honeymoons.com. A lifelong traveler, Jim's wanderlust has led him to spend months living on the Mayan Rivera, instruct SCUBA diving in Croatia, sail from San Diego to Hawaii, and cruise the Caribbean on a catamaran. Jim launched his honeymoon business while planning his own honeymoon in 2019. Since then, he has helped thousands of honeymooners plan their trips through his honeymoon travel agency .

Share This Article

June 1, 2020

Due to travel restrictions, plans are only available with travel dates on or after

Due to travel restrictions, plans are only available with effective start dates on or after

Ukraine; Belarus; Moldova, Republic of; North Korea, Democratic People's Rep; Russia; Israel

This is a test environment. Please proceed to AllianzTravelInsurance.com and remove all bookmarks or references to this site.

Use this tool to calculate all purchases like ski-lift passes, show tickets, or even rental equipment.

8 Honeymoon Travel Insurance Benefits You Need to Have

Get a Quote

{{travelBanText}} {{travelBanDateFormatted}}.

{{annualTravelBanText}} {{travelBanDateFormatted}}.

If your trip involves multiple destinations, please enter the destination where you’ll be spending the most time. It is not required to list all destinations on your policy.

Age of Traveler

Ages: {{quote.travelers_ages}}

If you were referred by a travel agent, enter the ACCAM number provided by your agent.

Travel Dates

{{quote.travel_dates ? quote.travel_dates : "Departure - Return" | formatDates}}

Plan Start Date

{{quote.start_date ? quote.start_date : "Date"}}

Share this Page

- {{errorMsgSendSocialEmail}}

Your browser does not support iframes.

Popular Travel Insurance Plans

- Annual Travel Insurance

- Cruise Insurance

- Domestic Travel Insurance

- International Travel Insurance

- Rental Car Insurance

View all of our travel insurance products

Terms, conditions, and exclusions apply. Please see your plan for full details. Benefits/Coverage may vary by state, and sublimits may apply.

Insurance benefits underwritten by BCS Insurance Company (OH, Administrative Office: 2 Mid America Plaza, Suite 200, Oakbrook Terrace, IL 60181), rated “A” (Excellent) by A.M. Best Co., under BCS Form No. 52.201 series or 52.401 series, or Jefferson Insurance Company (NY, Administrative Office: 9950 Mayland Drive, Richmond, VA 23233), rated “A+” (Superior) by A.M. Best Co., under Jefferson Form No. 101-C series or 101-P series, depending on your state of residence and plan chosen. A+ (Superior) and A (Excellent) are the 2nd and 3rd highest, respectively, of A.M. Best's 13 Financial Strength Ratings. Plans only available to U.S. residents and may not be available in all jurisdictions. Allianz Global Assistance and Allianz Travel Insurance are marks of AGA Service Company dba Allianz Global Assistance or its affiliates. Allianz Travel Insurance products are distributed by Allianz Global Assistance, the licensed producer and administrator of these plans and an affiliate of Jefferson Insurance Company. The insured shall not receive any special benefit or advantage due to the affiliation between AGA Service Company and Jefferson Insurance Company. Plans include insurance benefits and assistance services. Any Non-Insurance Assistance services purchased are provided through AGA Service Company. Except as expressly provided under your plan, you are responsible for charges you incur from third parties. Contact AGA Service Company at 800-284-8300 or 9950 Mayland Drive, Richmond, VA 23233 or [email protected] .

Return To Log In

Your session has expired. We are redirecting you to our sign-in page.

Frequently asked questions

About honey, honey products, our backing, contacting honey, joining honey, making payment, making changes, claims and your insurance policy, cyclone reinsurance pool, your privacy, industry information, insurance jargon, about homeowners insurance, optional benefits, about landlord insurance, about renters insurance, smart home program discount, installation and operation, troubleshooting, sensor support, who is honey.

Honey is smarter home insurance helping you prevent avoidable accidents. Rather than waiting for things to go wrong, we actively try and protect your home, with smart home sensors, from many of the common mishaps that lead to claims, like fire, theft and water damage. It’s an entirely new – and we like to think smarter – way of keeping your home and contents safer. We also use our smarts to take the guesstimating out of choosing your coverage – and to insure you in three minutes flat.

What makes Honey different?

Honey is Australia’s smart home insurance for the modern-day homeowner, renter or landlord, on a mission to eliminate the majority of avoidable accidents that happen in the home. We do this through a re-imagined approach to home insurance that lets customers easily sign-up with the right level of cover by using satellite and third party data, and then provide customers with smart home technology to help protect their homes.

What kind of products does Honey offer?

We protect you financially if something happens to your home or precious things. We offer three types of coverage with policy options to suit your needs:

Homeowners Insurance

For your primary residence - the place you live in and call home - we provide:

- Home cover - the building itself, as well as attached fixtures and fittings.

- Contents cover – your furniture, electrical appliances and personal belongings in the home, and as well as optionally some items you take outside your home.

- Combined Home and Contents cover – both of the above combined in one policy.

Renters Insurance

Where you are living in a home that you rent from someone else we provide:

- Contents cover – your furniture, electrical appliances and personal belongings in the home, as well as optionally some items you take outside your home.

Landlord Insurance

For an investment property you are renting out and not living in we provide:

- Building cover – the building itself, as well as attached fixtures and fittings.

- Contents cover – items owned by you left at the property for the tenants use such as furniture, blinds, curtains and carpets.

- Combined Building and Contents cover – both of the above combined in one policy.

Who is Honey backed by?

We’re backed and underwritten by RACQ Insurance – one of Australia’s most trusted brands, and supported by industry leaders such as AGL, Metricon, Mirvac and PEXA who invested in Honey.

Where can I access your Product Development and Sales Policy?

This is maintained by our underwriter, RACQ, and is available on their website here .

Where is Honey available?

From Brisbane to Bonnie Doon, Rottnest Island to the Red Centre, if you live anywhere in Australia, we’re available.

How do I contact Honey?

You can chat with our team by calling 137 137 between 8 am and 7 pm, Monday to Friday (Sydney time). Or, if you prefer, you can also email us at [email protected] . If your enquiry is urgent, it’s better to call. Email responses can take up to one business day.

How do I join Honey?

You can sign up for your quote, in 3 minutes right here .

How can I retrieve my quote?

When you get a quote, you have the option to send yourself a copy by email or SMS. And if you’ve provided us with your email address, we’ll automatically send through a copy as well. Use the links in either of these to retrieve your quote.

Will my application for insurance be accepted?

Sometimes we’ll need to chat with you before providing a quote or coverage. Leave it to us to get in touch in these cases, and we’ll simply ask a few more questions about you and your insurance needs. In the unlikely situation that we are not able to offer you any coverage at all, our team will be happy to discuss the details of the situation.

What should I do with my policy documents?

Within an hour of signing up, you’ll receive four important documents to your email:

- Your Certificate of Insurance

- Product Disclosure Statement (PDS)

- Any applicable Supplementary PDS

- Key Facts Sheet (KFS)

These documents tell you what you are and are not covered for, your excesses, limits and more. If there’s anything in your documents that you don’t understand or seems a bit off, call us on 137 137 . Once you’re good, pop your documents somewhere safe in case you need to refer back to them or make a claim.

Is there a cooling-off period?

You have a 21-day cooling-off period starting from the date and time we issue your policy or midnight on your renewal date. As long as you haven’t made a claim, you can cancel your policy within this time, and we’ll refund your premium in full.

How do I get replacement documents?

Your documents are always available online. You can get hold of them by logging into your account . You can also call us on 137 137 , and our team can email or post new copies to you. For the Product Disclosure Statement and other general documentation, you’re able to download them directly from our site.

How do I get a Certificate of Currency?

When you take out a policy we send you your Certificate of Insurance. However sometimes your bank or another institution will require a Certificate of Currency. Certificates of Currency are available online. You can access yours by logging into your account . You can also call us on 137 137 , and our team can email or post a copy to you. We can also send a Certificate of Currency directly to your financier. Have their details ready when you chat with us.

What is a cover note and do you offer them?

A cover note is a temporary document issued by an insurance company that provides proof of insurance coverage until a final insurance policy can be issued. A cover note is different from a certificate of insurance or an insurance policy document.

We don’t offer cover notes for Home, Contents or Landlord Insurance.

How often do I pay my premiums?

You can choose to pay annually or by the month, whatever suits you, at no extra charge.

How can I pay for my policy?

We debit your annual or monthly premium from a credit card or bank account.

For annual payments, you can select the date of your first payment, as long as it’s up to 30 days after your policy activation date.

For monthly payments, you choose the day of the month for the first and subsequent payments to be made.

What happens if my payment date falls on a weekend or public holiday?

If your nominated date falls on a non-business day, your payment will be taken out on the next business day.

Can I change my level of cover whenever I want?

We know life can be unpredictable, so we give you the flexibility to make changes to your cover during the policy period. If you want to request a change, call us as soon as you can on 137 137 . Changes are only effective from the time you notify us.

How do I update my direct debit details?

Give us a call on 137 137 , and our team will sort it out for you.

What should I do if I move house?

Moving can be a real headache, so we’ve made updating your insurance to a new home as simple and smart as possible. Before you move, give us a call on 137 137 to chat through all the details. We’ll need to know things like:

- The date you are moving

- Where you are moving to

- Details of your new home

Premiums are calculated based on where you live, so your new home might have a different premium than your old place.

Can I update my policy online?

Yes. You can log in to your account and update some details about your policy at honeyinsurance.com/my-account/

How do claims work?

Claiming is simple, sweet and smart. There are a few ways you can claim – both online and on the phone. For all the details, check out our Claims page. Whatever the issue, our team has your back.

How do I make a claim?

Our claims team is here for you, all day, every day. If you need to make a claim, you can lodge it online or speak with our team on 137 138 . We’re available 24/7/365. If you’re in an emergency and your home is damaged or under threat of damage, call the SES on 132 500 .

For more details, check out our Claims page.

What information do I need to make a claim?

To help us process your claim as quickly as possible, please have the following info handy when lodging your claim online or on the phone:

- Your policy number (it’s the number in your online reference or policy documents)

- The date and details of the incident

- A Police Report number for lost or stolen items

- Details of any damaged property or items that have been lost or stolen

- Proof of ownership of any damaged or stolen property (e.g. receipts, invoices or photographs)

- A damage report and quote for repairs of the damage

- Samples of damaged items such as carpet, blinds or rugs (only if it’s safe to get them)

- Contact details of any witnesses or other people involved

- Your paid invoices

- Photos of any damaged contents that are creating a health hazard

Your Certificate of Insurance has all the details of what you’re entitled to claim.

How do I contact Honey about an existing claim?

Our team gets in touch every 20 business days – at a minimum – to update you on the progress of your claim. If you need to chat about anything in the meantime, we’re here for you. Just give us a call on 137 138 .

Why do you need my receipts or proof of purchase?

These documents help us validate your claim and make sure we have all the info needed to process things quickly. If you can’t find your documents for some reason, we’ll work with you to find a way to keep your claim progressing and get everything finalised.

Who will manage my insurance claim?

Claims handling and settling services are provided by RACQ. To view the RACQ Claims Philosophy please click here .

For more information about the claims process please visit the RACQ Claims Website .

What is the Cyclone Reinsurance Pool?

The Cyclone Reinsurance Pool, developed by the Australian Reinsurance Pool Corporation (ARPC) allows Honey to help lower the cost of premiums for customers who live in areas where cyclones are common, such as North Queensland. The pool aims to make the cost of insurance more affordable for homes that have a high or medium risk of being affected by cyclones and cyclone-related flooding, and have relevant cyclone protection measures in place.

Isn’t cyclone cover already included in my policy?

Yes, Honey covers loss or damage to your home or contents caused by a storm, including cyclone. However, if you live in a cyclone-prone area, then you could be eligible for a lower premium under the Cyclone Reinsurance Pool.

How does the Cyclone Reinsurance Pool affect my insurance premium?

You could receive a reduction on your insurance premium if your home has had cyclone-grade resilience improvements or renovations made to it.

How does it affect my cover?

There won’t be any changes to what your policy covers.

Will the claims process change in the event of a cyclone?

There will be no change to how Honey customers will make a claim. The Honey claims team is here to support you through the same process as always.

Who is eligible to receive a lower premium?

New and renewing policies starting from 28th November 2023 in cyclone-impacted areas of Australia could be eligible for a lower premium if those customers:

- Hold a Honey Home Insurance policy

- Are located in an eligible postcode, such as coastal areas north of the Tropic of Capricorn

- Have eligible cyclone-grade protection measures

Can I still get a lower premium if I install cyclone protection at a later date?

If you have an existing and eligible Honey policy and your policy started or renewed from 28 November 2023, we can review your premium if eligible cyclone-grade protection measures are installed. Simply call our friendly team on 137 137 .

Are any of my personal details sold or disclosed to any third parties?

We comply with our obligations under Australian Privacy Law. Our Privacy Statement explains how we treat your personal information. This info is also detailed in our Product Disclosure Statement .

Are my bank and credit card details protected?

We take the collection and privacy of your details very seriously. All your financial details remain encrypted and secure once entered into our system. Our Privacy Statement explains how we treat your personal information.

How do I make a complaint?

We understand that sometimes we may not always meet your expectations and you may have a complaint. If this happens, we treat this seriously and have a process to deal with your complaint.

Making a complaint is a 3-step process

- Step 1: Talk to us by either calling on 137 137 or sending an email to [email protected] . We aim to acknowledge all complaints within 24 hours.

- Step 2: If you’re not happy with our response to your complaint, you can refer your complaint to our Internal Dispute Resolution Committee.

- Step 3: If you’re not happy with how our Internal Dispute Resolution Committee decides to resolve your complaint, you can refer it to the Australian Financial Complaints Authority [AFCA].

This is just a summary. The full details of our complaints and feedback process can be found here .

Insurance Fundamentals

What’s a premium.

A premium is the amount you pay to get insurance cover. It is the cost of your insurance policy.

How is my premium calculated?

Your premium is based on a number of things, including:

- What you choose to insure and how much you choose to insure it for

- Where your home is and risk information specific to your location (e.g., the likelihood of a flood, cyclone or bushfire, or crime rates in your suburb)

- Features specific to your home (e.g., building materials, the age of the building, and security features)

- The excess amount you have chosen

- Your claims history

In most cases, the higher the risk of loss or damage, the higher the insurance premium. The chance of loss or damage is different for everyone, so we calculate your premium based on your individual circumstances.

How can I reduce my premium?

You can reduce your premium by choosing a higher excess. Remember, though, that while your premium will be cheaper, you will have to pay a higher excess if you need to make a claim.

Where can I get general information about the insurance industry?

The Insurance Council of Australia has developed the Understanding Insurance website. It is designed to educate you about how insurance works.

What is the Emergency Services Levy (ESL)?

The Emergency Services Levy (ESL) is an emergency services insurance contribution scheme that funds the fire and rescue emergency services in New South Wales (NSW). Insurance companies are required to contribute to the budget for these services in NSW each financial year. Insurers may reclaim this amount from their policyholders by charging an ESL in their insurance policy premium.

The Emergency Services Levy Insurance Monitor (ESL Monitor) published an Order requiring insurance companies, and those acting on their behalf, to provide a breakdown of the ESL component of the premium, as well as year on year premium comparisons. These disclosure requirements are being enforced by the ESL Insurance Monitor.

Will the Emergency Services Levy increase insurance premiums?

There is no direct charge to policy premiums because of the Emergency Services Levy (ESL). But you may see an impact in the ESL contribution compared to last year. Want to know more? Check out the Revenue NSW website for information.

What’s the difference between an insurance company and a broker?

An insurance company can offer you a range of policies. You can use this information to purchase a policy from that insurance company. Brokers are professional advisors who have access to insurance policies from a range of insurance companies. They can provide you with advice on which policy is best suited to you, and they will purchase this policy from the insurance company on your behalf.

What does risk mean?

When we talk about risk, we are talking about the chances of an incident occurring that will cause damage or loss. All insurance companies calculate risk to determine a customer’s premium. It’s putting a financial value on the risk. When we assess and price risk, we are working out how much it would cost to replace and/or rebuild the insured item and the likelihood that this will occur in a period of insurance (i.e. one year).

For example, if you have a low-lying, single-story house on a waterway, your property could be considered a high flood risk.

We know it’s not that black and white. However, while we consider many other factors, both of these scenarios could result in a higher premium or additional excess.

What is underinsurance?

This is when the amount you are insured for on your Certificate of Insurance is below what it would cost to replace or rebuild. According to the Insurance Council of Australia, your property is considered to be underinsured if your insured amount covers less than 90% of the cost to rebuild.

For example, if your home is insured for $200,000, but it will cost $300,000 to rebuild it, you may not receive enough money from your insurance company to rebuild. Our smart calculators provide you options to help you work out how much you should insure your property for.

What is over-insurance?

Over-insurance is when you insure your property for more than it is worth. This does not mean you will get the inflated value if you make a claim. In the event of a successful claim, you can be paid the replacement value of the property lost or damaged.

For example, if your home is insured for $300,000 when it only costs $200,000 to rebuild, you may only receive $200,000 from your insurance company. Our smart calculators provide you options to help you work out how much you should insure your property for.

What is reinsurance?

Insurance companies need insurance as well. It’s call reinsurance. In the event of a major catastrophe, sometimes the amount of money we pay to help customers recover from loss or damage takes a large portion out of our reserves. By insuring a percentage of those reserves, we make sure that we can recover some of the money we pay out to customers. That way, we can continue to offer you a competitive premium.

What is Homeowners Insurance, and why is it important?

Homeowners Insurance can cover you for both your home’s building and contents in the case that they need repair, rebuilding or replacement after an insured event (a fancy way of saying something happened and then you need to make a claim). This includes protection from unpredictable weather and the impacts of cyclones, floods, storms and bushfires. Homeowners Insurance also protects you against things like theft, damage and legal liability.

What am I covered for?

Honey Homeowners Insurance covers your home and/or contents against loss or damage as a result of an insured event. For a full list of the insured events we cover, please refer to our Product Disclosure Statement .

Does Honey Insurance cover me for flooding?

We do. Our Product Disclosure Statement defines a flood as: The covering of normally dry land by water that has escaped or been released from the normal confines of any of the following:

- a lake, river, creek or other natural watercourse (whether or not it has been altered or modified)

- a reservoir, canal or dam

What am I not covered for?

For a full list of exclusions under your policy, please refer to the Product Disclosure Statement .

Am I covered immediately?

You’re covered from the date you requested your cover to start. However, if you don’t have existing insurance, we can’t cover you for fire or flood damage for 72 hours.

What is ‘new-for-old’ replacement?

We insure a new-for-old replacement on your belongings. This means that your covered possessions will be replaced with brand new items should something happen to them.

How much should I insure my home for?

While we aren’t able to provide you with advice on the replacement costs of your home or how much to insure it for, we use the information you give us and data sourced from third parties to recommend an amount of cover you should have. You should use this recommendation as a guide.

When considering how much you should insure your home for – often referred to as the sum insured – you should include: the full cost to rebuild your home, including the cost of structural improvements on the property. However, don’t include land value. Our policies include an allowance for demolition and site clearance, as well as professional fees. You should also consider increased building costs to meet any relevant local council building requirements. If you are unsure of the replacement cost, a builder or architect may be able to assist you.

We recommend that you use a home building calculator to determine independently an appropriate sum insured for your needs, which you can then compare to the guide provided by us during your quote.

How much should I insure my contents for?

We aren’t able to provide you with advice on the replacement costs of your contents or how much to insure it for. Instead, we use the information you give us and data sourced from third parties to recommend an amount of cover you should have. You should use this recommendation as a guide.

Your contents sum insured should include items such as fixtures and fittings (e.g. carpet, blinds, curtains), furniture, electrical goods, and all personal items. Items of value that you want to list on your Certificate of Insurance – such as jewellery, media or artworks – should also be included in the overall sum insured.

We recommend that you use a contents calculator to determine independently an appropriate sum insured for your needs, which you can then compare to the guide provided by us during your quote.

My contents aren’t worth that much. What is the point in having insurance cover?

Think about the items you wouldn’t be able to resume a regular day without, if these items had been stolen or damaged. What’s a home office without your laptop, your living room without your TV, or your shower without running water?

Another way of thinking about this is to consider the cost of replacing all of your items, rather than just their current value. In the event of a claim, and if you need to replace all your items, you may not have the money available to do so. This is why it’s recommended to have contents insurance.

Why do I need to list certain individual items on my policy?

Certain individual items such as valuables, collectibles and media have limits on how much they can be covered for. Details of this can be found in our Product Disclosure Statement . If you would like to be covered for the full replacement value of an item, let us know, and we’ll list it on your policy. You may need to provide proof of each item’s value at the time of a claim, so we recommend keeping receipts, valuations or proof of purchase.

What happens if I don’t list my valuables and they are stolen?

There are limits to how much some types of items can be covered for. If they’re not listed on your policy for the full value, they may be subject to the limits stated in our Product Disclosure Statement (PDS). Please check out the PDS for items that need to be listed, as well as the standard limits that apply.

If you need to make changes or list additional items under your policy, call us on 137 137 . Our team will sort it out quick smart.

Why has my home and contents sum insured increased on my renewal documents?

Each year when your policy renews, we automatically increase the amount you are insured for to keep your cover in line with the rate of inflation. In addition to this adjustment, you may also want to consider the value of any new contents or improvements to your home. If you need to make changes or list additional items, call us on 137 137 . Our team is on hand to help you out.

Can I get building insurance if my home is under strata title?

Normally, we can’t insure homes under strata title. They’re insured under a body corporate. There are a few instances where we can offer building insurance for strata title properties. We may also be able to offer contents insurance to cover any fittings and fixtures that aren’t covered as part of the strata insurance. If you are unsure, give us a buzz on 137 137 . Our team will be happy to chat things through with you.

What is strata title?

Strata title is a title based on dividing the site into lots with separate titles. The most common application of strata title is for units, but it is also used for complexes with a number of duplexes and villas.

What is the Advanced Cover option, and what does it cover?

Advanced Cover is available on home and contents insurance policies. It provides cover for both Accidental Damage and Motor Burnout.

What does Accidental Damage cover?

Though we do our best to protect you from accidents, we know they’re still going to happen. Accidental Damage cover protects you in the event that you accidentally damage your home or contents.

For example, if you are moving furniture around the house and damage your wall, or if you spill a drink that damages your carpet, you could be protected under the Accidental Damage option. For full details of conditions and exclusions, check out our Product Disclosure Statement .

What does Motor Burnout cover?

Motor Burnout covers you for damage caused by an electrical current that results in the burnout of a household electrical motor. Examples of items that have electric motors are ducted air conditioning, pool pumps and refrigerators. For full details of conditions and exclusions, check out our Product Disclosure Statement .

What’s an excess?

An excess is the amount you are required to pay towards a claim on your policy. When you take out a policy, we apply a standard excess. On most of our policies, you can select your excess from a range of options to increase or decrease your premium. A higher excess reduces your premium and costs you more at claim time. A lower excess increases your premium but lowers your costs at claim time. The choice is entirely yours based on what’s appropriate for you.

Why do I have to pay an excess?

An excess is payable for all claims made against your policy – unless we state otherwise in the Product Disclosure Statement (PDS). Excesses on insurance policies help keep premiums down by reducing the number of small claims made. The amount and type of excess you have to pay will be shown on your policy schedule. For full conditions and exclusions relevant to your policy, check out your policy schedule or PDS.

How do I find out my Homeowners Insurance excess?

You can find your nominated excess on your home and/or contents Certificate of Insurance. That document is sent to you by email when you first take out your policy or when your policy is renewed. If you can’t find your Certificate of Insurance, please call us on 137 137 . Our team is here to help.

Can I change my excess?

You can increase your excess at any time during the policy period. You can only decrease your excess when renewing your policy or within the 21-day cooling-off period – provided you have not made a claim.

How does my excess impact the premium I pay?

An excess is the amount you contribute towards claims. This means if you’re willing to contribute more at the time of a claim – paying a higher excess – you will generally have a lower premium during the policy period.

If there’s damage to my home and contents, do I pay two excesses if I lodge a claim?

If your claim is a result of the same insured event and the damage sustained is due to the same insured event – e.g. damage to both your home and contents as a result of the same storm – then you will only need to pay one excess, whichever is the higher of the two.

Landlord Insurance

What is landlord insurance and why is it important.

Landlord Insurance can cover both the building and the contents of your investment property in the case that they need repair, rebuilding, or replacement after an insured event (a fancy way of saying something happened and then you need to make a claim). This includes protection from unpredictable weather and the impacts of cyclones, floods, storms, and bushfires. Landlord Insurance can also protect you against things like theft or damage by a tenant, lost rent, and legal liability.

What’s the difference between Landlord and Homeowners Insurance?

There are several differences between Landlord and Homeowners Insurance, the main difference being that Landlord Insurance provides protection for an investment property you are renting out and not living in, whilst Homeowners Insurance is for your primary residence – the place you live in and call home.

Homeowners Insurance covers the home and contents of the house you permanently live in (commonly called a “dwelling”), the things (contents) in your house, and your liability related to the property. It does not cover the risks that come with having a tenant living at your property, such as tenant damage and rent default, making insurance for landlords relevant to cover any property that you permanently rent out.

I already have Honey Homeowners Insurance, do I need Landlord Insurance too?

Firstly, it’s great that you have made Honey Insurance the cover for your primary residence – the place you live in and call home. Landlord Insurance should not be used to cover your primary residence, however if you have an investment property Honey Landlord Insurance could be for you. Landlord Insurance can protect your investment property from the risks that come with having a tenant living at your property. Additionally, if you’ve borrowed money to buy your investment property, your financial institution may require you to take out insurance on the property.

Do I need content insurance as a landlord?

There are a few situations where you may want to consider contents insurance as a landlord to make sure you have appropriate cover.

For example, if your property is an apartment, townhouse or unit and is covered by insurance under a strata title that policy may not cover everything that you would like covered. For example, fixtures and fittings such as the kitchen cupboards and appliances, as well as carpets, curtains and blinds may not be covered within your strata insurance policy. A strata policy is also unlikely to provide cover for the risks associated with a tenant living in your property such as loss of rent and tenant damage. You should check this and consider a landlord content policy.

Where your investment property is a free-standing house, look beyond the building. Whether the property is fully furnished, has a couple of big-ticket items (a refrigerator, a washing machine etc), or nothing at all but the carpet and curtains – contents insurance may be suitable for you as a landlord.

Landlord Insurance can cover your investment property building and/or contents against loss or damage as a result of insured events such as theft or vandalism, floods, fires and storms to mention a few. Landlord Insurance can include building, contents or combined building and contents cover.

Building cover provides cover for the building and structures not under strata title, outdoor items such as fixed water tanks, barbecues and solar panels, and indoor items like walls, ceilings and floors. It can also provide cover for fixtures and fittings such as carpets, curtains and blinds. Contents cover for landlords can cover things like electrical appliances, your furniture and furnishings within the property, lawn and garden equipment and unfixed swimming pools.

Landlord Insurance also provides cover for many of the specific risks that come with renting out your property to a tenant. This includes cover for accidental or malicious damage caused by the tenant, rent default and loss of rent due to the property being impacted by an insured event.

For a full list of the insured events and coverages, as well as terms, conditions and any applicable limits please refer to our Product Disclosure Statement .

We do. Our Product Disclosure Statement defines a flood as: The covering of normally dry land by water that has escaped or been released from the normal confines of any of the following: a lake, river, creek or other natural watercourse (whether or not it has been altered or modified) a reservoir, canal or dam. Please refer to the PDS as certain conditions and exclusions apply.

For a full list of exclusions under your policy, please refer to the Product Disclosure Statement .

You’re covered from the date you requested your cover to start. However, if you don’t have existing insurance, we can’t cover you for flood, water runoff, bushfire, storm surge or storm damage for 72 hours.

Honey Landlord Insurance provides new-for-old replacement on your belongings. This means that your possessions will be replaced with brand new items should something happen to them. Because they wear and tear, unfortunately, carpets over 10 years old are not covered with new for old.

How much should I insure my investment property for?

We aren’t able to provide you with advice on the replacement costs of your investment property or how much to insure it for. Instead, we use the information you give us and data sourced from third parties to suggest an amount of cover you should have. You should use this suggestion as a guide.

When considering how much you should insure your investment property for – often referred to as the sum insured – you should include the full cost to rebuild your investment property, including the cost of structural improvements on the property. But don’t include land value. Our policies include an allowance for demolition and site clearance, as well as professional fees for the design of your replacement home. You should also consider increased building costs to meet any relevant local council building requirements. If you are unsure of the replacement cost, a builder or architect may be able to assist you.

We recommend that you use a property building calculator to determine independently an appropriate sum insured for your needs, which you can then compare to the guide provided by us during your quote. Keep in mind that policies receive 5% of the building sum insured for fixtures and fittings.

Can I get landlord building insurance if my property is under strata title?

Normally, we can’t insure the building of an investment property under strata title. They’re insured under a body corporate. We do offer contents insurance to cover any fittings and fixtures that aren’t covered as part of the strata insurance. If you are unsure, give us a call on 137 137 . Our team will be happy to chat things through with you.

Am I covered if my tenant defaults on their rent payments?

If you take out a Landlord insurance policy with Honey, when your tenant is in default, we may pay the net rental income up to 10% of your sum insured. If your building is damaged to an extent that the tenant can’t live in it, or access to use your building is not possible due to damage to the property or strata title development, we may pay for loss of rent on the insured property for the time it is unoccupied. This benefit is automatically included in your policy and subject to terms and conditions in the Product Disclosure Statement .

Am I covered if my property becomes unoccupied?

Your property can continue to be covered under a Honey Landlord policy against insured events even if it becomes unoccupied. You may be required to pay an additional excess if something happens, but you can rest easy knowing the property is covered.

We consider your rental property unoccupied if no one has been living in it for more than 60 consecutive days or if someone stays there on average for less than one night a week during the 60 day period.

Am I covered if I’m renovating?

Until the roof, floor and external walls are in place, we don’t cover loss or damage to your rental property (and building materials) or your contents caused by events detailed in the Product Disclosure Statement .

Is Landlord Insurance tax deductible?

In some cases, yes. Be sure to check with your tax adviser to find out whether you can claim a tax deduction for your Landlord Insurance costs.

If your investment property is leased as a rental property, you may be able to claim Landlord Insurance costs for your rental property for the period it was tenanted or available for rent.

Am I covered if my rental property becomes untenantable because of storm damage?

Yes. When your property is being repaired after an insured event such as flood, fire, or storm damage, and your tenant can’t live at the property our Landlord insurance policy will pay the net rental income up to 10% of your sum insured.

Am I covered without a lease agreement?

We cannot cover you without a lease agreement. You must have a rental agreement between you and the tenant, and we require that you have it managed by a licensed property manager.

Will Honey cover my holiday rental?

Right now, we are unable to cover homes rented for short-term holiday purposes (less than 3 months) with our Landlord insurance. However, you may be able to find a suitable home or contents policy for your holiday rental on the Insurance Council of Australia website, Find an Insurer .

What’s the difference between a short-term and long-term rental?

A long-term rental is a formal lease where the entire property is rented out as a residence for a minimum period of 3 months. A short-term rental (if you allow guests to accommodate your property registered with a provider like Airbnb) is where you rent the entire property to paying guests for short-term holiday purposes. This rental period under a casual let must be less than 3 months.

Can I choose my own repairer for my property repairs?

We have a specialist panel of repairers who help our customers nationally and are able to safely assess, repair or rebuild your home. As part of this process, we’ll share all information openly with you and, where you’d like to discuss an alternative action such as choosing a different repairer or being paid a fair and reasonable amount for the repairs, our Claims team will gladly support that.

Can I get smart home sensors with Landlord Insurance?

At this time, we do not offer smart home sensors with our Landlord Insurance policy. However, we’ll be sure to update all policyholders if this changes.

Does Honey offer Motor Burnout cover?

Motor Burnout is available as an optional benefit on building and contents insurance policies. By adding Motor Burnout cover you can be covered for loss or damage to the electric motors in your major electric appliances if they burn-out and stop working - provided they are less than 10 years old.

How do I find out my Landlord Insurance excess?

You can find your nominated excess on your building and/or contents Certificate of Insurance. That document is sent to you by email when you first take out your policy or when your policy is renewed. If you can’t find your Certificate of Insurance, please call us on 137 137 . Our team is here to help.

If there’s damage to my investment property building and contents, do I pay two excesses if I lodge a claim?

If your claim is a result of the same insured event and the damage sustained is due to the same insured event – e.g. damage to both the building and your contents as a result of the same storm – then you will only need to pay one excess, whichever is the higher of the two.

What is Renters Insurance, and why is it important?